portfolioafterlife

too fast for love

In Turchia esplode la inflazione, ecco la disamina della situazione, a causa di politiche economiche e monetarie non corrette.

Charlie Munger once said, “It’s not greed that drives the world, but envy.”

awealthofcommonsense.com

awealthofcommonsense.com

What it takes to be a successful active investor. Hint, it’s much harder than you think.

Contrast active and passive equity investing. Risk/rewards.

Conclusion—Investors who do not have the following traits and emotional quality should index their portfolios. I find they are the majority of investors today. Also discussion of points of failure for passive and active investors.

What traits and emotional characteristics are required to succeed as an active investor?

A true long-term perspective on their investments.

Discussion of Evolution and why it hampers long-term thinking.

Discussion of behavioral biases that hamper successful long-term active investing.

Power Point illustrations.

Successful active investors value process over outcome.

Short-term focus of investors is killing returns.

Why you need access to truly long-term data to make intelligent choice.

Successful active investors generally ignore forecasts and predictions.

Discussion of studies proving forecasts and predictions are virtually worthless; illustrations documenting the failure of forecasts; both within markets and in outside professions.

Successful active investors are patient and persistent.

Discussion of great investors who may have very different styles, but all share the trait of patience and persistence.

Successful active investors have a strong mental attitude.

Successful investors are made, not born. Discussion of how successful active investors have a mental attitude bordering on stoicism; how they control how they interpret the world.

Tools to use to help you succeed as an active long-term investor.

Long-term data uncovered by What Works on Wall Street that you can use to guide your investment strategy.

The importance of value; momentum; financial strength and earnings quality in putting together your portfolio.

A highlight of stocks with high versus low shareholder yield (Cash dividend %+Bet Buyback %); it’s efficacy since the 1920s

What NOT to own, lottery stocks versus the market.

The importance of a stock’s market capitalization—the most profitable stocks come from the smallest part of the market (Micro cap stocks)

Putting it all together—should you be an active or passive investor?

Weight of the evidence for passive and active investing

Which type of investor are you? Getting the best out of the style you choose.

Discussion and Q/A.

Description:

What role, exactly, do skill and luck play in our successes and failures? Some games, like roulette and the lottery, are pure luck. Others, like chess, exist at the other end of the spectrum, relying almost wholly on players' skill.

In his provocative book, Michael Mauboussin untangles the intricate strands of skill and luck, defines them, and provides useful frameworks for analyzing their relative contributions. He offers concrete suggestions for how to put these insights to work to your advantage in business and other dimensions of life.

About the author:

Michael J. Mauboussin is a Managing Director and Head of Global Financial Strategies at Credit Suisse. Prior to rejoining CS in 2013, he was Chief Investment Strategist at Legg Mason Capital Management. He is also the author of three books, including More Than You Know: Finding Financial Wisdom in Unconventional Places, named in the The 100 Best Business Books of All Time by 800-CEO-Read. Michael has been an adjunct professor of finance at Columbia Business School since 1993, and received the Dean's Award for Teaching Excellence in 2009. He is also chairman of the board of trustees of the Santa Fe Institute, a leading center for mulch-disciplinary research in complex systems theory.

The study showed that the top 10,000 bitcoin accounts hold 5 million bitcoins, an equivalent of approximately $232 billion.

With an estimated 114 million people globally holding the cryptocurrency, according to crypto.com, that means that approximately 0.01% of bitcoin holders control 27% of the 19 million bitcoin in circulation.

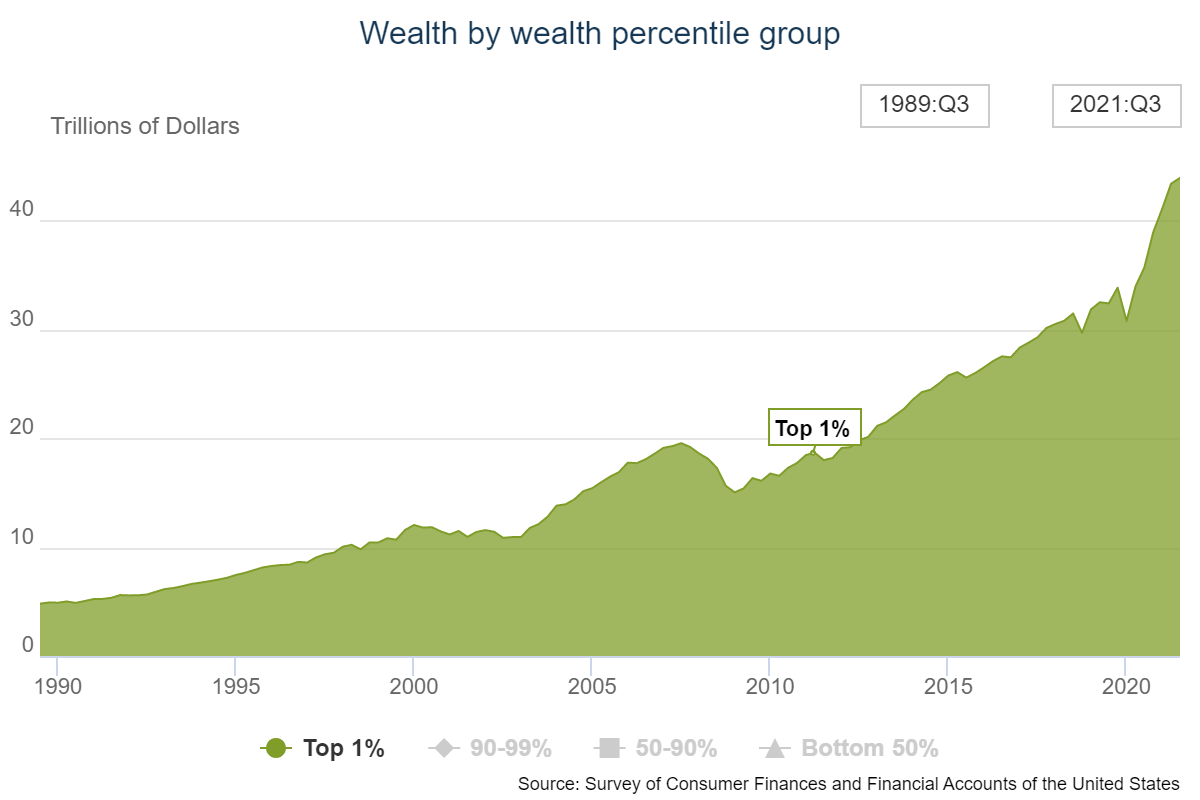

By comparison, in the U.S., where wealth inequality is at its most extreme in decades, the top 1% of households hold about a third of all wealth, according to the Federal Reserve.

The ramifications of that centralization are mainly twofold, the paper argues. First, it makes the entire bitcoin network more susceptible to systemic risk. Second, it means the majority of the gains from the rising price and increased adoption go to a disproportionately small group of investors.

www.wsj.com

www.wsj.com

")

www.evidenceinvestor.com

www.evidenceinvestor.com

Unlikely bedfellows? Both Russell 1000 Growth and Russell 2000 Value have nearly identical % gains YTD, despite latter outpacing former in 1H21 [Past performance is no guarantee of future results]

boglecenter.net

boglecenter.net