paologorgo

Chapter 11

Morningstar analyst Todd Lukasik expects a flurry of purchase activity in the commercial real estate space, starting now and then intensifying in 2011 and 2012.

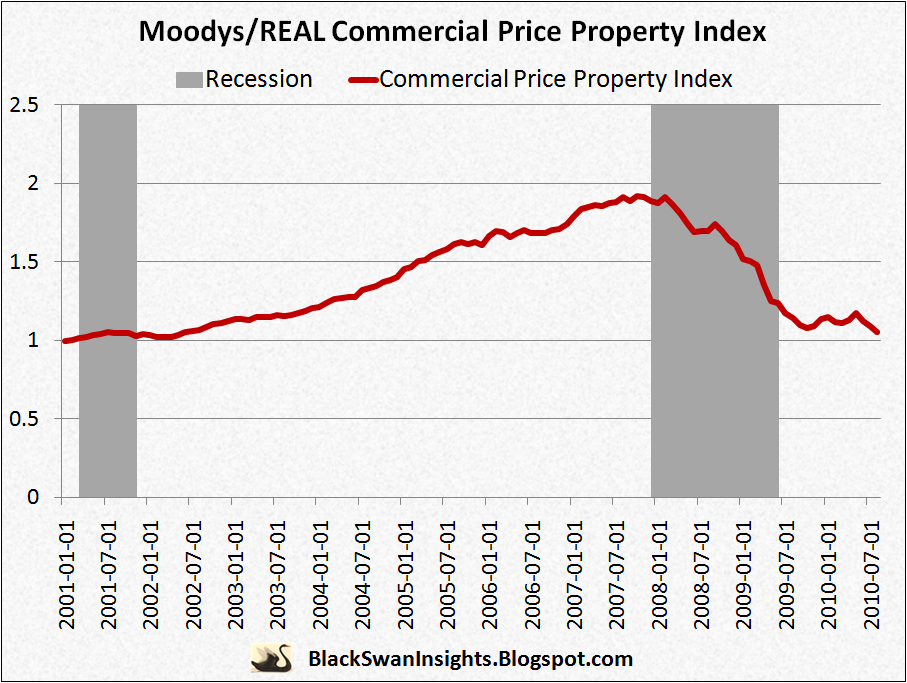

It's not so much that the commercial real estate market is healthy, but rather that there will be massive amounts of distressed properties as many property owners' untenable debt burdens come due. (For more background, see a previous post here)

Investment capital has been massing on the sidelines, waiting for the inevitable buying opportunities which will arise.

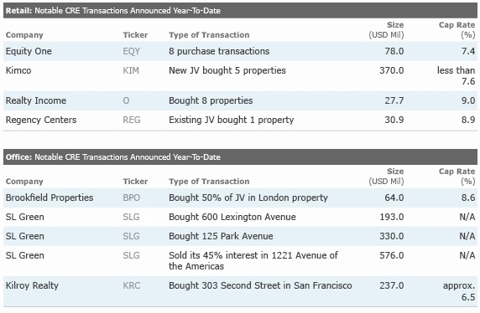

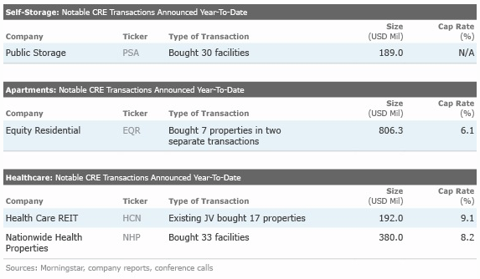

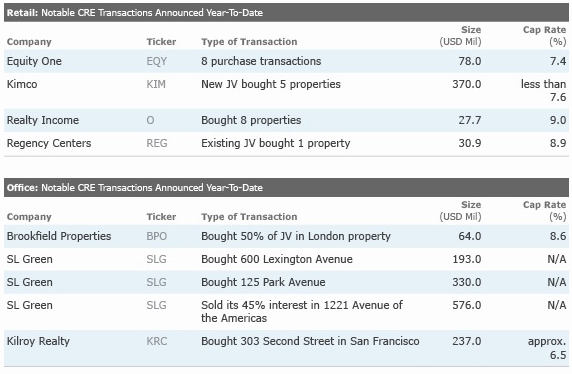

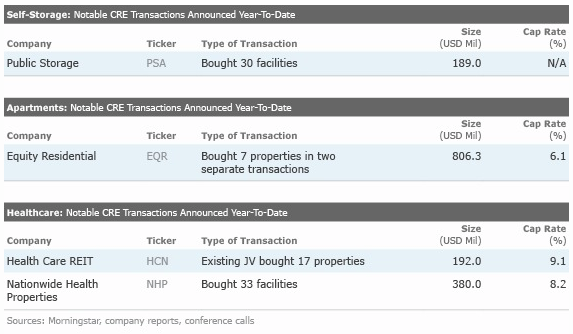

In fact, transaction activity has already begun to pick up as shown by the Morningstar tables below (click to enlarge images):

This is just the tip of the iceberg. You'd be forgiven if you underestimated the scale of new capital which will be required by distressed commercial real estate companies over the next few years:

Morningstar:

It's not so much that the commercial real estate market is healthy, but rather that there will be massive amounts of distressed properties as many property owners' untenable debt burdens come due. (For more background, see a previous post here)

Investment capital has been massing on the sidelines, waiting for the inevitable buying opportunities which will arise.

In fact, transaction activity has already begun to pick up as shown by the Morningstar tables below (click to enlarge images):

This is just the tip of the iceberg. You'd be forgiven if you underestimated the scale of new capital which will be required by distressed commercial real estate companies over the next few years:

Morningstar:

In its February report, the Congressional Oversight Panel concluded that about $700 billion in commercial real estate loans that come due between 2010 and 2014 are underwater. We think a sizable amount of the additional $700 billion in commercial real estate loans coming due during that time frame are loans that could not get refinanced at existing levels in the current lending environment. This suggests that there are at least hundreds of billions of dollars of incremental equity capital that need to be injected into commercial real estate to establish a "proper" leverage level. In fact, The Real Estate Roundtable, an industry group comprised of representatives from public and private real estate firms, has estimated this equity gap at about $1 trillion over the longer term.

We believe the industry's need to deleverage over the coming years will create an environment that fosters outright asset sales and joint venture transactions. We expect 2011 and 2012 to be particularly active years, as that's when many of the loans made in 2006 and 2007--years when property prices and lenders' risk appetites were simultaneously peaking--will start to come due

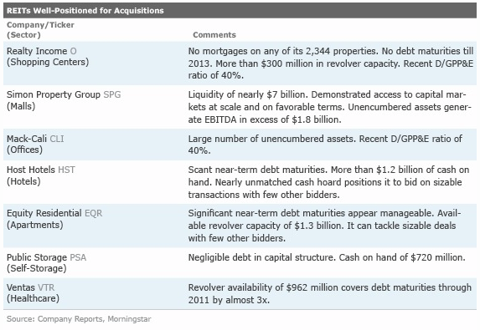

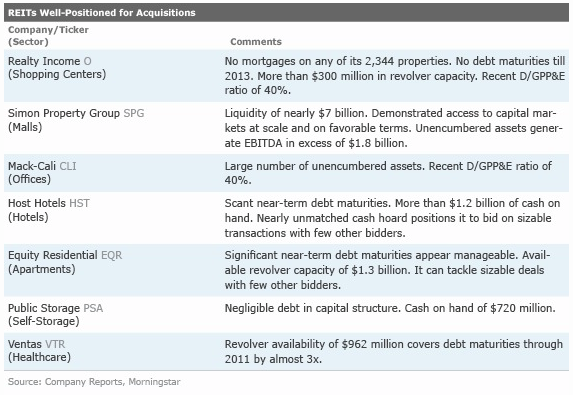

Thus it will be a great time for property investors with the capacity to acquire assets, ie. those that didn't take on too much leverage previously, or fresh players. Here are some key REIT picks from Mr. Lukasik:

http://seekingalpha.com/article/210290-commercial-real-estate-needs-significant-new-capital-to-be-bailed-outWe believe the industry's need to deleverage over the coming years will create an environment that fosters outright asset sales and joint venture transactions. We expect 2011 and 2012 to be particularly active years, as that's when many of the loans made in 2006 and 2007--years when property prices and lenders' risk appetites were simultaneously peaking--will start to come due

Thus it will be a great time for property investors with the capacity to acquire assets, ie. those that didn't take on too much leverage previously, or fresh players. Here are some key REIT picks from Mr. Lukasik:

")