paologorgo

Chapter 11

Equinix è leader nel settore della colocation, ed ha appena acquisito il suo più grosso competitor nel mercato americano.

Le quotazioni sono molto elevate (priced for perfection), ma il settore continua ad avere tassi di crescita elevati, anche in periodo di crisi, che lo rendono estremamente interessante.

Da Seeking Alpha:

Equinix (EQIX) will be reporting 2Q 2010 results on Wednesday, July 28th. This call will be particularly interesting as Equinix completed the acquisition of Switch and Data in the quarter - while we do not expect that the two Companies might have already developed significant synergies, we are sure that the conference call will be useful to give investors additional color on the status of the integration.

According to its updated guidance given on May 7, Equinix expects revenues to be in the range of $296.0 to $298.0 million, with cash gross margins of about 64%. This forecast reflects a closing date of April 30, 2010 for the Switch and Data acquisition, which therefore will contribute to Equinix’s results from May 1, 2010 onwards only.

As a side note, the strength of the US dollar (or, said in a different way, the recent weakness of the Euro, which represented about 16% of revenues for the former stand alone Equinix) might have negatively impacted Equinix's non-US results for the quarter, as guidance was given using, for example, $1.36 dollar to the euro.

On a same currency basis, we expect Equinix's performance in Europe and Asia to show very good strength, in spite of currency conversions.

Analysts estimate revenues of 295.9M on average, slightly below Company's guidance, and EPS of $ 0.24.

The strategic importance of the Switch and Data merger deserves spending a good part of this article reviewing, once more, the reasons behind the acquisition and its potential impact on Equinix numbers/synergies going forward.

Equinix's recent “Update Call on Closure of Switch and Data Acquisition” comes in handy:

The comment about the additional capacity is interesting, as Equinix, with this acquisition, has basically doubled the number of cabinets available for sale in the North American market.

We believe that the impact of this new inventory will start producing positive effect mostly in the second half of 2010:

In our opinion, the New York metro area will strongly benefit from the combination of the Switch and Data inventory and the great success that Equinix is achieving within the financial vertical (comment added in Italic):

Equinix has recently been in the news for several wins within the financial community, like Deutsche Börse Systems, selecting Equinix as strategic data center provider in Frankfurt, Germany and the Australian Securities Exchange, operator of the Australian futures market, deploying its new hosting solution within the Equinix Chicago (CH1) data center. Several networks have also announced connections to different Equinix's data centers worldwide, targeting the low latency needs of financial institutions. As a reminder, Equinix is the only colo provider with a presence at all major exchange markets worldwide.

Focusing on the New York market, Direct Edge has just converted its trading platforms to formal Exchanges, and is now operating from the Equinix NY4 data center, a move which could represent an important catalyst for the financial community.

These comments are taken from Securities Technology Monitor:

More information about the Direct Edge Exchange come from wallstreetandtech.com:

From an interconnection stand point, Equinix has increased the number of networks and ISPs connected to its data centers from 410 to 575. Switch and Data's success in network density was unparalleled in the industry, and approximately 31% of revenues were represented by interconnection services, or more than double Equinix numbers. Switch and Data Palo Alto and Equinix Ashburn represent the two most important peering points on the West and East Coast of the USA, and both Company’s regional data centers will benefit from the wider offer of ISPs and networks that they will now be able to offer to their existing customers base.

From a financial point of view, Equinix will take advantage of Switch and Data'S NOLs, and expects to generate about $20 million of synergy savings within one year, which is quite a substantial amount, if we consider that it does represent about 10% of Switch and Data cash costs.

Equinix is also estimating acquisition costs of about $23 million for professional and legal fees, that will be split between 2009 and 2010. Integration costs will also be substantial:

As some key operating metrics were used in slightly different ways by the two Companies, Equinix provided a reconciliation sheet on its web side for Switch and Data's recent quarter.

As far as revenues, Equinix hasn't really included any synergy in its forecast:

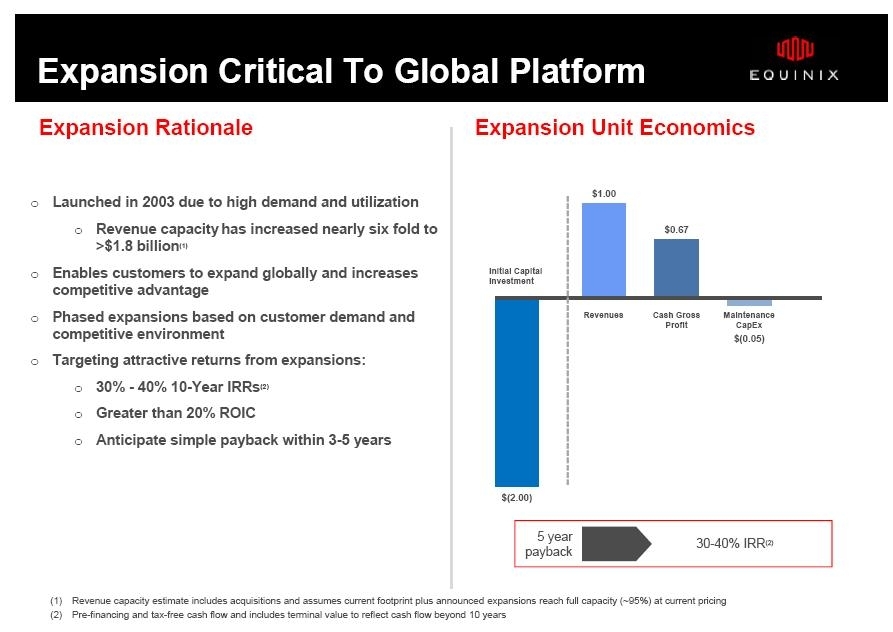

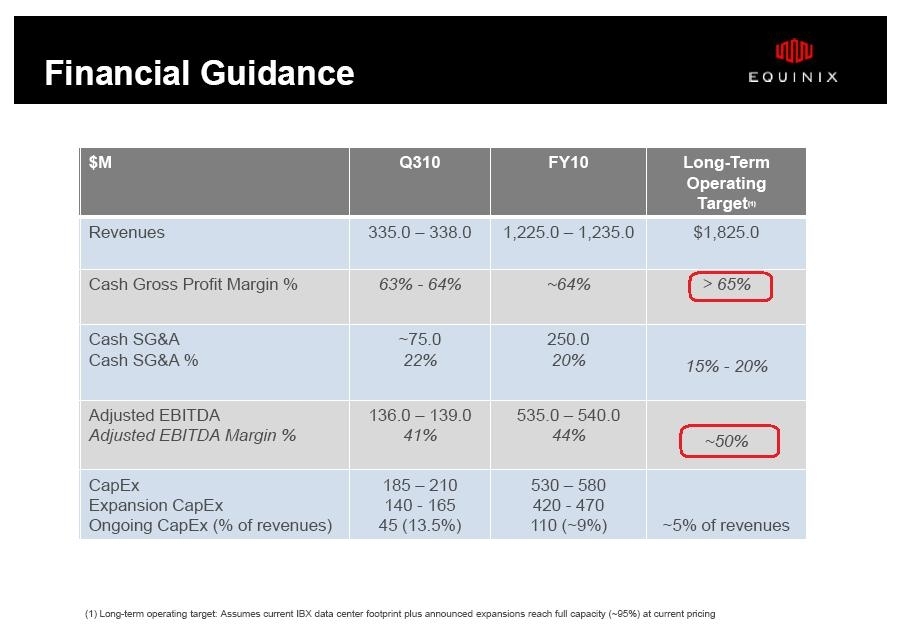

The combined business would be already in a position to generate about 1.8 billion of revenues, excluding further expansions that the now combined Company might need to take into consideration quickly:

Disclosure: Long EQIX

Le quotazioni sono molto elevate (priced for perfection), ma il settore continua ad avere tassi di crescita elevati, anche in periodo di crisi, che lo rendono estremamente interessante.

Da Seeking Alpha:

Equinix (EQIX) will be reporting 2Q 2010 results on Wednesday, July 28th. This call will be particularly interesting as Equinix completed the acquisition of Switch and Data in the quarter - while we do not expect that the two Companies might have already developed significant synergies, we are sure that the conference call will be useful to give investors additional color on the status of the integration.

According to its updated guidance given on May 7, Equinix expects revenues to be in the range of $296.0 to $298.0 million, with cash gross margins of about 64%. This forecast reflects a closing date of April 30, 2010 for the Switch and Data acquisition, which therefore will contribute to Equinix’s results from May 1, 2010 onwards only.

As a side note, the strength of the US dollar (or, said in a different way, the recent weakness of the Euro, which represented about 16% of revenues for the former stand alone Equinix) might have negatively impacted Equinix's non-US results for the quarter, as guidance was given using, for example, $1.36 dollar to the euro.

On a same currency basis, we expect Equinix's performance in Europe and Asia to show very good strength, in spite of currency conversions.

Analysts estimate revenues of 295.9M on average, slightly below Company's guidance, and EPS of $ 0.24.

The strategic importance of the Switch and Data merger deserves spending a good part of this article reviewing, once more, the reasons behind the acquisition and its potential impact on Equinix numbers/synergies going forward.

Equinix's recent “Update Call on Closure of Switch and Data Acquisition” comes in handy:

The strategic rationale for this acquisition centers around five key elements. Gaining a quick entry in new markets, securing additional capacity in our existing markets, enhancing our core focus on network density and interconnection services, and producing strong financial synergies to enhance the accretiveness of this transaction. Finally this transaction continues to distance Equinix from other data center providers, and further establishes us as the only global network neutral data center provider, and clearly with the largest North American footprint. -- Steve Smith, Equinix Inc. President, CEO

We believe that the impact of this new inventory will start producing positive effect mostly in the second half of 2010:

Secondly, we will drive top-line growth with a strong focus on achieving revenue synergies across both sales organizations. An early sign of success over the past week is that we have already identified several Equinix customers that are interested in the Switch & Data inventory, and we have also started to receive inbound lead opportunities to cross-sell Switch & Data customers into Equinix's global footprint.

In the New York metro area, we have now acquired three data centers in New York City, two of which are located within key telecom landing points. Additionally, the capacity gain from their sizable new data center in Bergen County, will supplement our existing footprint in New Jersey, which we expect to be important in meeting the demand from our financial services customer base.

Given our historical fill rates in this metro, we are very excited by the additional capacity in both New Jersey locations (the former Switch and Data Bergen facility and the new Equinix NY4 third phase expansion).

Given our historical fill rates in this metro, we are very excited by the additional capacity in both New Jersey locations (the former Switch and Data Bergen facility and the new Equinix NY4 third phase expansion).

Focusing on the New York market, Direct Edge has just converted its trading platforms to formal Exchanges, and is now operating from the Equinix NY4 data center, a move which could represent an important catalyst for the financial community.

These comments are taken from Securities Technology Monitor:

In 2,500 square feet of space, you can house a typical Radio Shack store, with hundreds of electronic products, ranging from smart phones to car security systems to MP3 players to weather radios to cables and batteries.

Or, in roughly the same amount of space, you can house a stock exchange. Or two.

Such is the case with EDGA and EDGX, the two newly approved stock exchanges owned by Direct Edge, which formally debut Wednesday in Secaucus, N.J. As competition in securities trading venues goes up, so does the drive for speed and “scalability,’’ the ability to expand rapidly and reliably.

…

Unlike the New York Stock Exchange, you won’t see a monster-sized flag draped over where Direct Edge operates the new trading platforms that will power EDGA and EDGX. The two exchanges sit side by side, in a black wire cage inside a nondescript industrial building that could just as easily hide a distribution warehouse.

Spare servers in this cage provide immediate backup, in case of failure. A second cage with copies of the entire EDGA and EDGX trading exchanges sits in another nondescript building in North New Jersey, just in case.

...

From the get-go, the new system will be able to handle 220,000 messages every second, while keeping up the pace of acknowledging each order in less than half a million. Each of the two exchanges can handle 2.5 billion transactions a day. “That is four times the capacity of even the days surrounding the Flash Crash,’’ said O’Brien. “So there is significant head room there.”

...

“There is no theoretical limit” to the amount of transactions Direct Edge will be able to handle each day, Bonanno said, at these speeds.

Or, in roughly the same amount of space, you can house a stock exchange. Or two.

Such is the case with EDGA and EDGX, the two newly approved stock exchanges owned by Direct Edge, which formally debut Wednesday in Secaucus, N.J. As competition in securities trading venues goes up, so does the drive for speed and “scalability,’’ the ability to expand rapidly and reliably.

…

Unlike the New York Stock Exchange, you won’t see a monster-sized flag draped over where Direct Edge operates the new trading platforms that will power EDGA and EDGX. The two exchanges sit side by side, in a black wire cage inside a nondescript industrial building that could just as easily hide a distribution warehouse.

Spare servers in this cage provide immediate backup, in case of failure. A second cage with copies of the entire EDGA and EDGX trading exchanges sits in another nondescript building in North New Jersey, just in case.

...

From the get-go, the new system will be able to handle 220,000 messages every second, while keeping up the pace of acknowledging each order in less than half a million. Each of the two exchanges can handle 2.5 billion transactions a day. “That is four times the capacity of even the days surrounding the Flash Crash,’’ said O’Brien. “So there is significant head room there.”

...

“There is no theoretical limit” to the amount of transactions Direct Edge will be able to handle each day, Bonanno said, at these speeds.

Direct Edge Chief Executive William O'Brien said the company is not about to venture into unfamiliar territory with its exchange status, which means tighter regulatory oversight.

But he said a new data center launched during the conversion opens a new battle front with competitors in selling trading data to increasingly hungry investors.

"That's something we view as a way to broaden our competitive footprint," O'Brien said in an interview. "As great as this company has progressed so far, I still feel like it is still getting started."

Just hours before ringing the exchanges' opening bell in Jersey City Wednesday, O'Brien told Reuters Insider that Direct Edge "could potentially" list its shares in an initial public offering. The IPO plan was originally set for this year.

But he said a new data center launched during the conversion opens a new battle front with competitors in selling trading data to increasingly hungry investors.

"That's something we view as a way to broaden our competitive footprint," O'Brien said in an interview. "As great as this company has progressed so far, I still feel like it is still getting started."

Just hours before ringing the exchanges' opening bell in Jersey City Wednesday, O'Brien told Reuters Insider that Direct Edge "could potentially" list its shares in an initial public offering. The IPO plan was originally set for this year.

From a financial point of view, Equinix will take advantage of Switch and Data'S NOLs, and expects to generate about $20 million of synergy savings within one year, which is quite a substantial amount, if we consider that it does represent about 10% of Switch and Data cash costs.

Equinix is also estimating acquisition costs of about $23 million for professional and legal fees, that will be split between 2009 and 2010. Integration costs will also be substantial:

For each of the quarters through the integration period, we will provide you an estimate of what we believe the integration costs to be, and compare those costs against the savings attributed to our synergies. For 2010 we expect the integration costs to be $2 million greater that the cost savings relating to the synergies. But as we looked at the entire integration period, as Steve mentioned, we expect to receive a minimum of $20 million in annual cost savings from this transaction, half of those annualized savings should be realized by the end of the year. The restructuring costs associated with this deal will primarily be incurred over the next three or four quarters, and will be expensed to the income statement on a separate income statement line. The restructuring costs will not affect our adjusted EBITDA metric. -- Keith Taylor, Equinix Inc. CFO

As far as revenues, Equinix hasn't really included any synergy in its forecast:

David Barden - BofA Merrill Lynch - Analyst

But no revenue synergies in the guidance at all?

Keith Taylor - Equinix Inc. - CFO

At this stage we haven't.

Clearly there is some expectation, again, as Steve alluded to, that we are already starting selling into their assets, and I understand from our sales team we are getting leads from the Switch and Data team into our (global) assets. So I think that there is going to be a strong opportunity for us. I think it will create some synergies, but we have not made that assumption today.

But no revenue synergies in the guidance at all?

Keith Taylor - Equinix Inc. - CFO

At this stage we haven't.

Clearly there is some expectation, again, as Steve alluded to, that we are already starting selling into their assets, and I understand from our sales team we are getting leads from the Switch and Data team into our (global) assets. So I think that there is going to be a strong opportunity for us. I think it will create some synergies, but we have not made that assumption today.

Yes, they actually, they do have a couple of projects that they have had under review, and we need to make decisions pretty much in the next 30 to 60 days, but given the commonality of the businesses and the markets we are focused on, they are projects we are very interested in, and we would like to pull right into our portfolio. So we see some good opportunities for expansion. -- Mark Adams, Equinix Inc., Chief Development Officer

")

")