paologorgo

Chapter 11

Equity markets might have recovered today, but there is still a gorilla in the room. The authors Carmen Reinhart and Kenneth Rogoff wrote the book, “[ame="http://www.amazon.com/gp/product/0691142165?ie=UTF8&tag=surly-20&linkCode=xm2&creativeASIN=0691142165"]This Time is Different: Eight Centuries of Financial Folly[/ame]” which is filled with a vast amount of historical statistics related to financial crises. The premise is simple: We have been here before. The size or subtle nuances of crises might be different, but they have a consistent flavor to them. In the case of Greece, it seems like a broken record. According to the authors, “Greece’s default on debt reached a nearly pandemic recurrence at the turn of the century… Greece has been in default roughly one out of every two years since it first gained independence in the nineteenth century.”

We always think this time is different and usually err on the side of optimism, otherwise, how else would we lend to a country that repeatedly goes bad on its debts? The credit default swap markets seem to see the writing on the wall for Greece and Portugal:

CDS Levels on Greece have hit an all time high of 6.38%

CDS Levels on Greece have hit an all time high of 6.38%

Portugal's CDS levels have hit an all time high of 2.76%

Portugal's CDS levels have hit an all time high of 2.76%

The Euro is looking worse and worse every day with further speculation of default contagion:

The Euro is collapsing versus the dollar, breaking down into new territory

The Euro is collapsing versus the dollar, breaking down into new territory

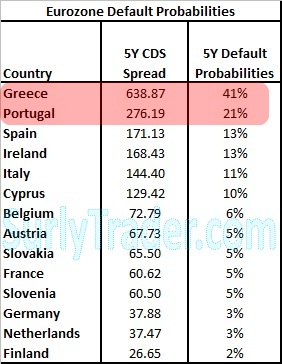

Greece and Portugal have 41% and 21% 5 year default probabilities respectively

This data speaks for itself. Either a massive bailout needs to occur against the wishes of German and French citizens, Greece and Portugal must leave the Eurozone, or the Euro must depreciate massively.

As food for thought, I will leave you with a rather insightful passage from “[ame="http://www.amazon.com/gp/product/0691142165?ie=UTF8&tag=surly-20&linkCode=xm2&creativeASIN=0691142165"]This Time is Different[/ame]“:

“The essence of this-time-is-different syndrome is simple. It is rooted in the firmly held belief that financial crises are things that happen to other people in other countries at other times; crises do not happen to us, here and now. We are doing things better, we are smarter, we have learned from past mistakes. The old rules of valuation no longer apply. The current boom, unlike the many booms that preceded catastrophic collapses in the past (even in our country), is built on sound fundamentals, structural reforms, technological innovations, and good policy. Or so the story goes.”

Sovereign Default – This Time is Not Different | SurlyTrader

We always think this time is different and usually err on the side of optimism, otherwise, how else would we lend to a country that repeatedly goes bad on its debts? The credit default swap markets seem to see the writing on the wall for Greece and Portugal:

CDS Levels on Greece have hit an all time high of 6.38%

Portugal's CDS levels have hit an all time high of 2.76%The Euro is looking worse and worse every day with further speculation of default contagion:

The Euro is collapsing versus the dollar, breaking down into new territory

Greece and Portugal have 41% and 21% 5 year default probabilities respectively

This data speaks for itself. Either a massive bailout needs to occur against the wishes of German and French citizens, Greece and Portugal must leave the Eurozone, or the Euro must depreciate massively.

As food for thought, I will leave you with a rather insightful passage from “[ame="http://www.amazon.com/gp/product/0691142165?ie=UTF8&tag=surly-20&linkCode=xm2&creativeASIN=0691142165"]This Time is Different[/ame]“:

“The essence of this-time-is-different syndrome is simple. It is rooted in the firmly held belief that financial crises are things that happen to other people in other countries at other times; crises do not happen to us, here and now. We are doing things better, we are smarter, we have learned from past mistakes. The old rules of valuation no longer apply. The current boom, unlike the many booms that preceded catastrophic collapses in the past (even in our country), is built on sound fundamentals, structural reforms, technological innovations, and good policy. Or so the story goes.”

Sovereign Default – This Time is Not Different | SurlyTrader

")

.

. Giuseppe

Giuseppe