paologorgo

Chapter 11

PROPERTY VALUES: 10 KEY CHARTS

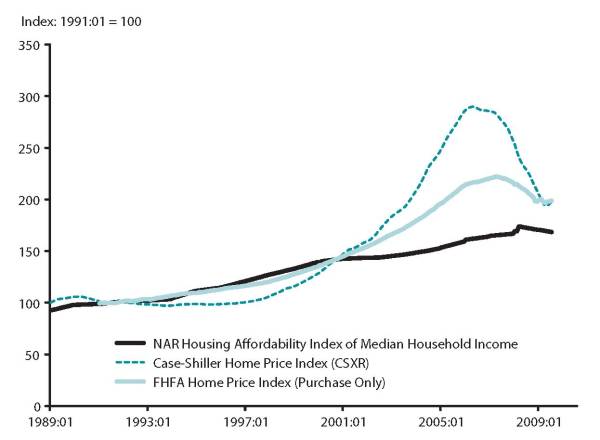

Affordability / GREEN BULLETS: There is good news in property values, although I have been warned about the accuracy of these numbers. My take: They can’t be completely inaccurate. For the would-be buyer who likes what he sees in this picture, ask yourself first: Do I want a good deal on my home purchase or do I want a great deal? If you can get a good deal now, it’s not going away soon. There may be a great deal in the future — say the next year or two or three. It will be gone if you buy the good deal today.

Affordability / GREEN BULLETS: There is good news in property values, although I have been warned about the accuracy of these numbers. My take: They can’t be completely inaccurate. For the would-be buyer who likes what he sees in this picture, ask yourself first: Do I want a good deal on my home purchase or do I want a great deal? If you can get a good deal now, it’s not going away soon. There may be a great deal in the future — say the next year or two or three. It will be gone if you buy the good deal today.

Inventory: Green Vomit (9/25): How could anybody say this is a reasonable time to invest in real estate? You could either prove these numbers wrong, or you could check into the mental ward. Have you had your medication today?

Macroeconomics: DEBT BE NOT PROUD (8/11/09): One school of thought says excess debt must be paid off or written off before we will achieve dynamic growth. This “Low Debt” and “High Debt” chart of approximately the last 60 years shows that the magnitude of debt, whether it be corporate or household, could be far beyond reasonable. If this school is correct, then we may have many years or even a decade of slow growth. The only cure would be radical steps to reduce debt. If we are in the hang over of a world-record credit bubble, then the outlook for real estate investment is negative.

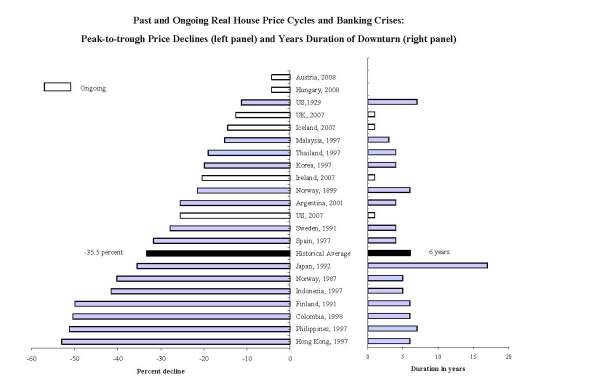

MacroEconomics: HISTORY’S TRENDS: The best research into credit bubbles says that property’s value will fall through the summer of 2012 — until three years from now. The good news is that the fall in values has nearly equalled the average fall of 35%. The bad news? What if we have a King-Kong credit bubble and it’s actually not stupid to say “It’s different this time.”?

Mortgage Performance / DELINQUENCY FREQUENCY: If distressed sales are the leading contributor to falling property values, then we have only just begun — TO FALL. This chart shows a quarter by quarter bubble blowing up in delinquent mortgages. 7 million mortgage accounts are now delinquent.

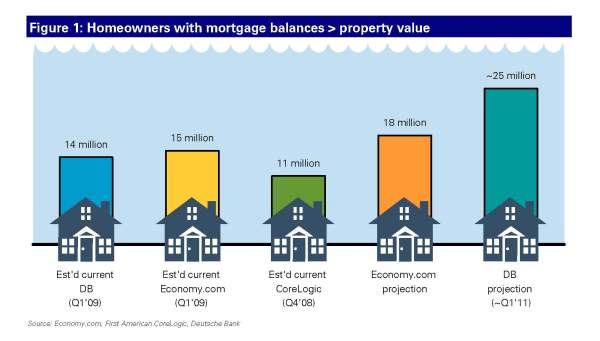

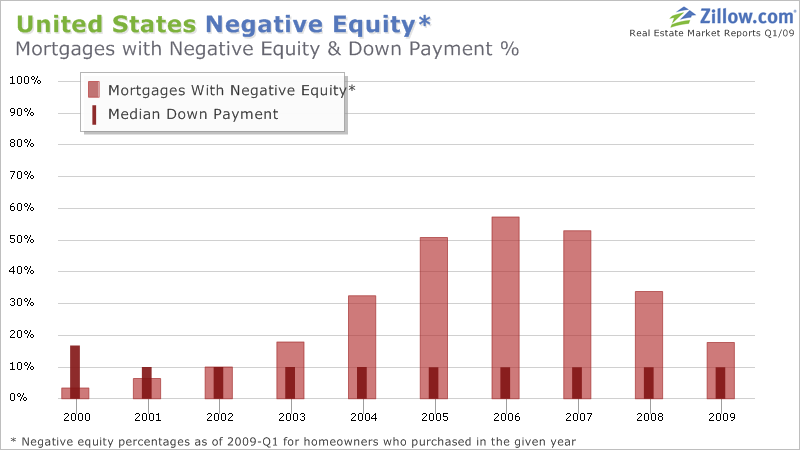

Mortgage Performance / Negative Equity – The Ten-Ton Gorilla: How many homeowners would make money by walking away from their mortgage and their home? Whether the number is 11 million or 25 million, the low and the high estimates in this graph, the risk factor is wildly high for prospectiv purchasers. How high? It’s like Cheech & Chong on Spring Break in Cancun.

Mortgage Performance / Negative Equity – The Ten-Ton Gorilla: How many homeowners would make money by walking away from their mortgage and their home? Whether the number is 11 million or 25 million, the low and the high estimates in this graph, the risk factor is wildly high for prospectiv purchasers. How high? It’s like Cheech & Chong on Spring Break in Cancun.

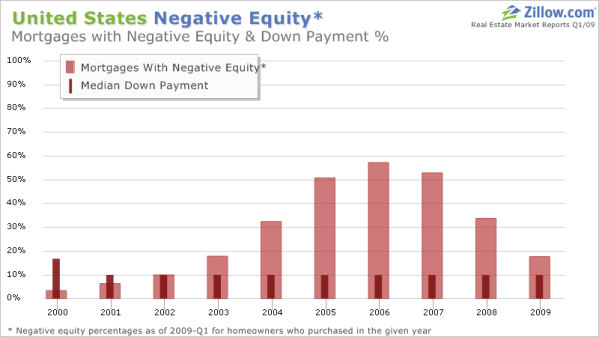

Mortgage Performance: NEGATIVE EQUITY (8/6/09): The graph shows half of all mortgages issued in 2006 have a balance greater than the value of the house securing the loan. What will happen to loan performance if 50% of all mortgages are worth more than their collateral? Nobody knows, and if nobody knows, then a wild massive risk factor cannot be forecast. If you think that is impossible, please note that Deutsche Bank issued a report in early August saying that 48% of all mortgages would be worth more than their collateral by 2011. This is unchartered territory adjacent to the galaxy beyond the next universe.

Mortgage Performance: PAYMENT STRIKE: Foreclosure sales are a leading source of falling values. Payment performance on mortgages is terrible and getting worse. More than 4% of mortgages are in foreclosure. More than 13% of mortgages (ONE IN EIGHT) are behind. There is no indication of a turn-around in current payments on mortgages. How does optimism make sense of this payment history?

Mortgage Performance: PAYMENT STRIKE: Foreclosure sales are a leading source of falling values. Payment performance on mortgages is terrible and getting worse. More than 4% of mortgages are in foreclosure. More than 13% of mortgages (ONE IN EIGHT) are behind. There is no indication of a turn-around in current payments on mortgages. How does optimism make sense of this payment history?

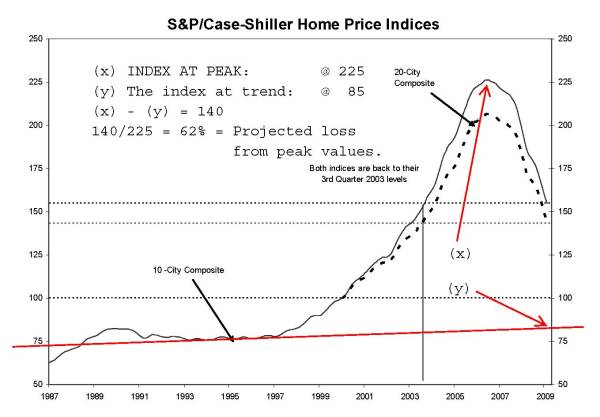

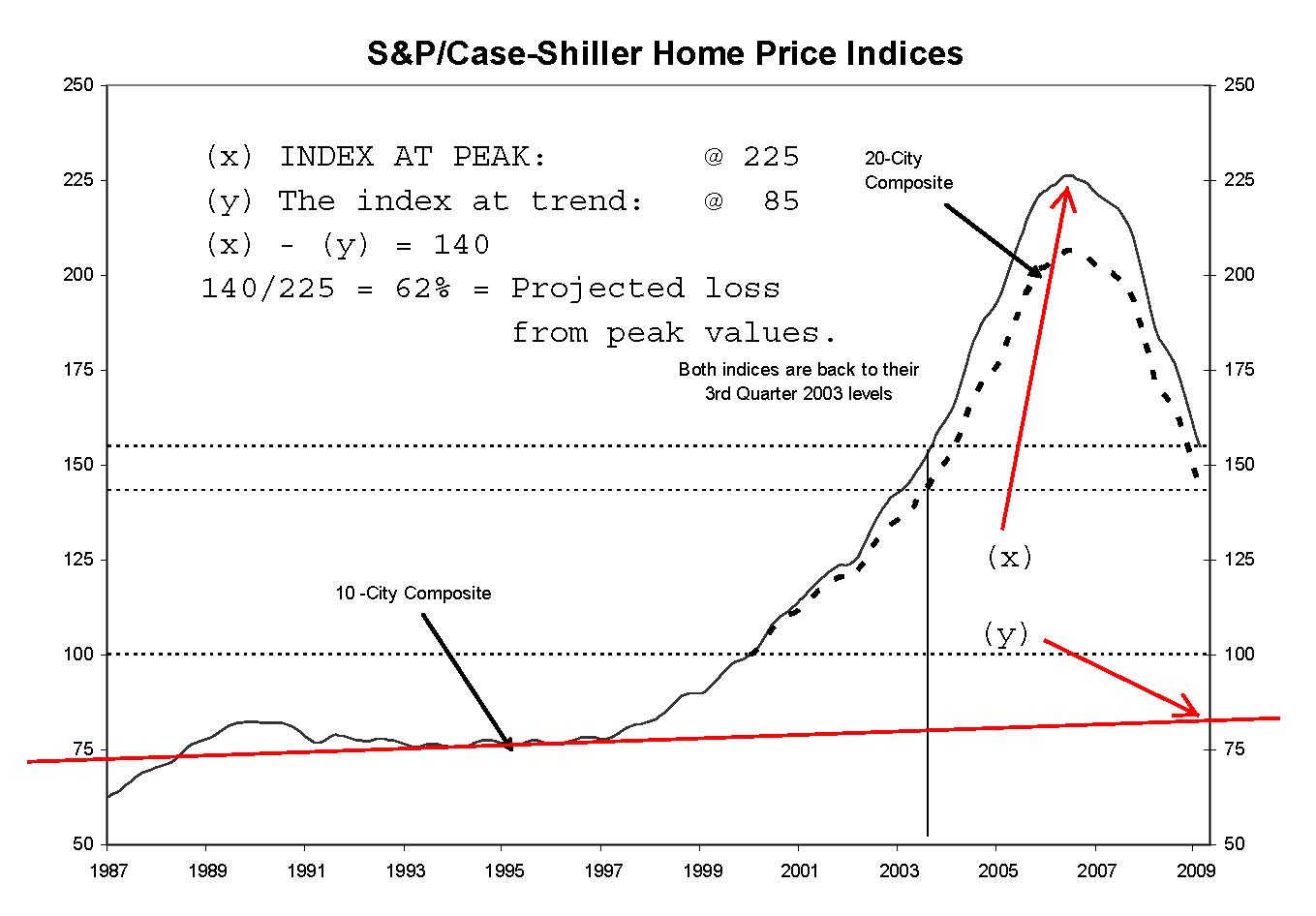

Price Trends: THE FALLING KNIFE: There is a lot of good news in the stock market today, but sentiment would turn 180 degrees if it was known that property values would fall 60% from their peak. Prices have already fallen @ 30%. If values fall according to the estimates in this graph, it is a certainty that banks and financial companies will fail en masse (again). There has been some good news about real estate prices lately, but the vast majority of indicators are still negative.

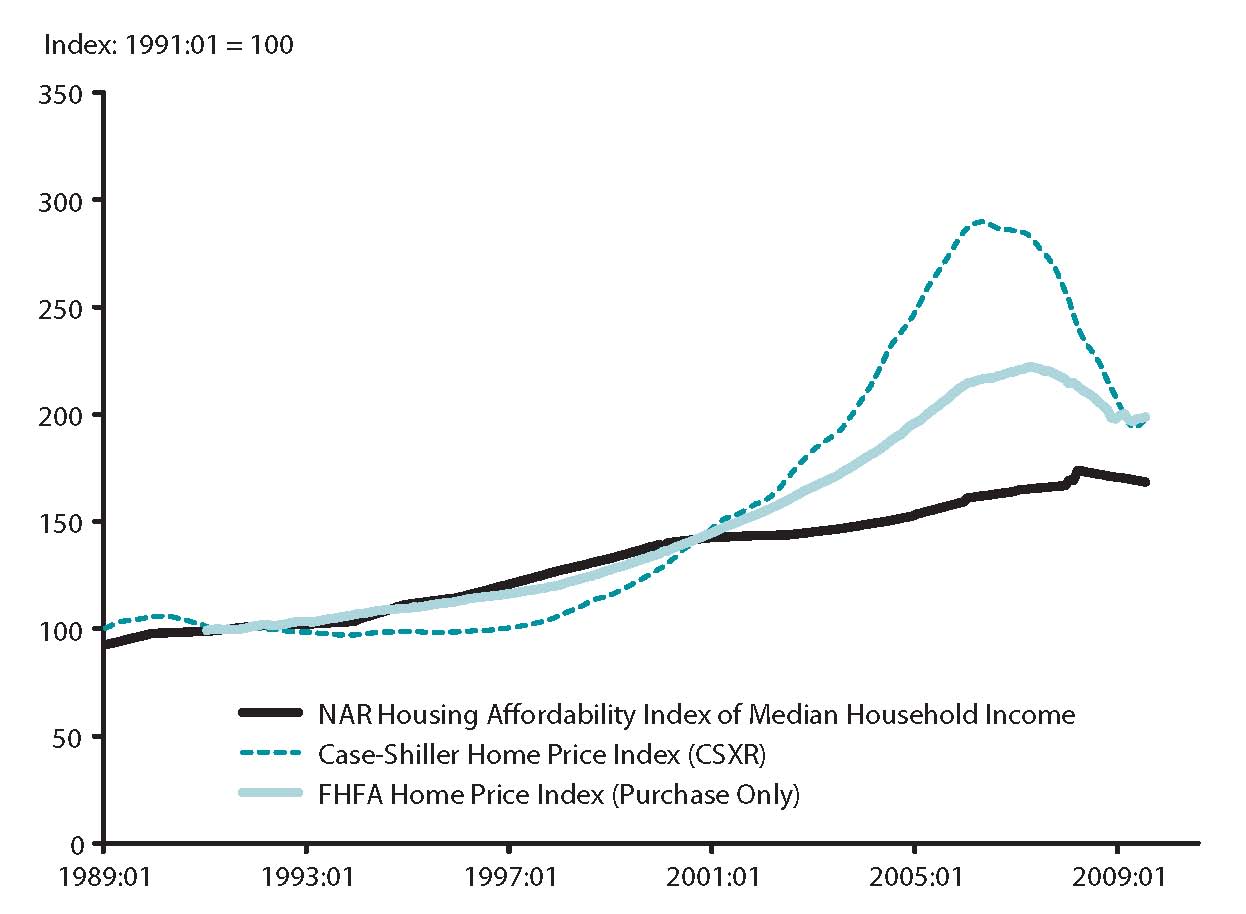

Price Trends: CONFUSION REIGNS: Here is one picture of price trends based upon 20 years of data. You can’t really make sense of it without a trend line. Please see graphs immediately above and below.

Price Trends: CONFUSION REIGNS: Here is one picture of price trends based upon 20 years of data. You can’t really make sense of it without a trend line. Please see graphs immediately above and below.

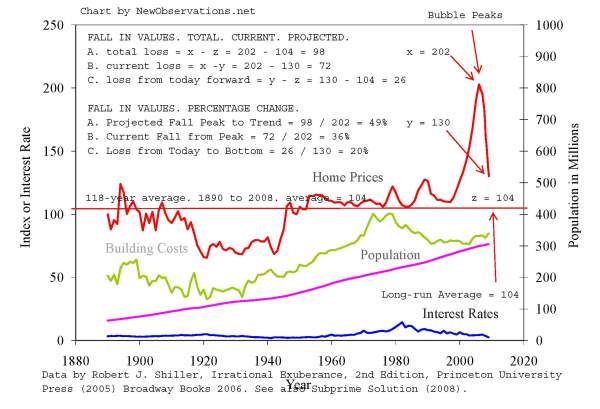

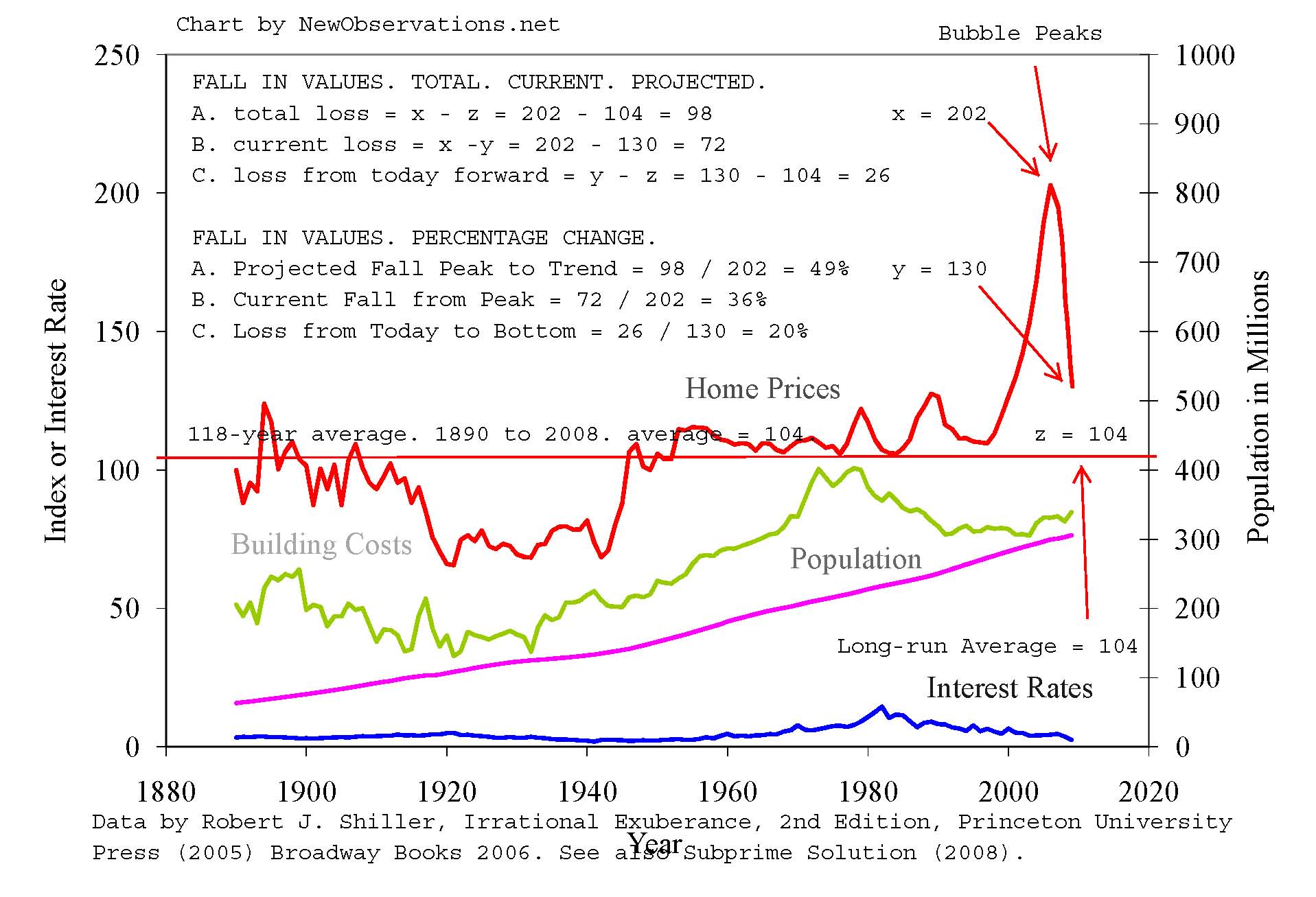

Price Trends / War of the Worlds (Part 2): We still have 20% to fall nationally. That’s on this chart. On another one it is 43%.

Price Trends / EQUITY VANISHES: About $7 trillion has been taken from the wealth account of property owners. If there are 130 million housing units in the United States (rental and owner occupied), then owners have lost an average of $54,000 per unit they own. The loss is massive.

Price Trends / EQUITY VANISHES: About $7 trillion has been taken from the wealth account of property owners. If there are 130 million housing units in the United States (rental and owner occupied), then owners have lost an average of $54,000 per unit they own. The loss is massive.

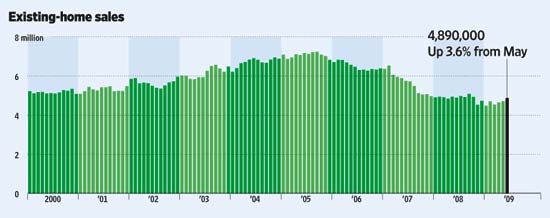

SALES -UNITS: Looking at the long trend, there has never been a serious problem in terms of the number of units sold. The quality of the sales is another question. The Wall Street Journal recently reported that two-thirds of sales are a form of distressed sale (Improving Home Sales Belie Market Reality, 8/21/09). “‘Think about that for a minute,’ John Mauldin of Millennium Wave Advisors wrote this week. ‘Two-thirds of home sales are either foreclosures or banks taking a loss on the mortgage.’ And only a third of the remaining one-third — roughly 10% of overall sales — comes from ’something we could call a normal selling process.’”

SALES -UNITS: Looking at the long trend, there has never been a serious problem in terms of the number of units sold. The quality of the sales is another question. The Wall Street Journal recently reported that two-thirds of sales are a form of distressed sale (Improving Home Sales Belie Market Reality, 8/21/09). “‘Think about that for a minute,’ John Mauldin of Millennium Wave Advisors wrote this week. ‘Two-thirds of home sales are either foreclosures or banks taking a loss on the mortgage.’ And only a third of the remaining one-third — roughly 10% of overall sales — comes from ’something we could call a normal selling process.’”

Michael David White, CEO of The New Mortgage Company, is a mortgage broker in Chicago. He blogs at NewObsrvations.net.

PROPERTY VALUES: 10 KEY CHARTS

- Before you buy a home, check here for recent charts on affordability, inventory, macroeconomic trends, mortgage-payment performance, price trends, and sales in units. It will open your eyes for your most important financial decision.

Inventory: Green Vomit (9/25): How could anybody say this is a reasonable time to invest in real estate? You could either prove these numbers wrong, or you could check into the mental ward. Have you had your medication today?

Macroeconomics: DEBT BE NOT PROUD (8/11/09): One school of thought says excess debt must be paid off or written off before we will achieve dynamic growth. This “Low Debt” and “High Debt” chart of approximately the last 60 years shows that the magnitude of debt, whether it be corporate or household, could be far beyond reasonable. If this school is correct, then we may have many years or even a decade of slow growth. The only cure would be radical steps to reduce debt. If we are in the hang over of a world-record credit bubble, then the outlook for real estate investment is negative.

MacroEconomics: HISTORY’S TRENDS: The best research into credit bubbles says that property’s value will fall through the summer of 2012 — until three years from now. The good news is that the fall in values has nearly equalled the average fall of 35%. The bad news? What if we have a King-Kong credit bubble and it’s actually not stupid to say “It’s different this time.”?

Mortgage Performance / DELINQUENCY FREQUENCY: If distressed sales are the leading contributor to falling property values, then we have only just begun — TO FALL. This chart shows a quarter by quarter bubble blowing up in delinquent mortgages. 7 million mortgage accounts are now delinquent.

Mortgage Performance: NEGATIVE EQUITY (8/6/09): The graph shows half of all mortgages issued in 2006 have a balance greater than the value of the house securing the loan. What will happen to loan performance if 50% of all mortgages are worth more than their collateral? Nobody knows, and if nobody knows, then a wild massive risk factor cannot be forecast. If you think that is impossible, please note that Deutsche Bank issued a report in early August saying that 48% of all mortgages would be worth more than their collateral by 2011. This is unchartered territory adjacent to the galaxy beyond the next universe.

Price Trends: THE FALLING KNIFE: There is a lot of good news in the stock market today, but sentiment would turn 180 degrees if it was known that property values would fall 60% from their peak. Prices have already fallen @ 30%. If values fall according to the estimates in this graph, it is a certainty that banks and financial companies will fail en masse (again). There has been some good news about real estate prices lately, but the vast majority of indicators are still negative.

Price Trends / War of the Worlds (Part 2): We still have 20% to fall nationally. That’s on this chart. On another one it is 43%.

SALES -UNITS: Looking at the long trend, there has never been a serious problem in terms of the number of units sold. The quality of the sales is another question. The Wall Street Journal recently reported that two-thirds of sales are a form of distressed sale (Improving Home Sales Belie Market Reality, 8/21/09). “‘Think about that for a minute,’ John Mauldin of Millennium Wave Advisors wrote this week. ‘Two-thirds of home sales are either foreclosures or banks taking a loss on the mortgage.’ And only a third of the remaining one-third — roughly 10% of overall sales — comes from ’something we could call a normal selling process.’”

SALES -UNITS: Looking at the long trend, there has never been a serious problem in terms of the number of units sold. The quality of the sales is another question. The Wall Street Journal recently reported that two-thirds of sales are a form of distressed sale (Improving Home Sales Belie Market Reality, 8/21/09). “‘Think about that for a minute,’ John Mauldin of Millennium Wave Advisors wrote this week. ‘Two-thirds of home sales are either foreclosures or banks taking a loss on the mortgage.’ And only a third of the remaining one-third — roughly 10% of overall sales — comes from ’something we could call a normal selling process.’”Michael David White, CEO of The New Mortgage Company, is a mortgage broker in Chicago. He blogs at NewObsrvations.net.

PROPERTY VALUES: 10 KEY CHARTS

")